Rates were recently increased by 75 basis points by the Federal Reserve, which just announced another significant rate increase. These adjustments aim to reduce inflation to manageable levels, but they also have an impact on other sectors of the economy. While increasing interest rates may increase the cost of borrowing, investors might benefit from greater profits on the balances of high-yield savings accounts.

Average interest rates on high-yield savings accounts are now at 3% APY, but some experts believe they might rise as high as 4% APY this year.

The information in this article will help you sort through some of the issues related to a savings bank account whether you are one of those people who store money in a savings account or are just getting ready to start saving money.

What are Interest Rates?

The yearly percentage of your balance that the bank pays you for maintaining money in your account is known as your interest rate when it comes to savings accounts. It is frequently referred to as a savings interest rate for this reason.

Why then does the savings rate in your savings account fluctuate between low and high? The Federal Reserve, or simply The Fed, is one of the causes. It among other things establishes monetary policy. Changes in interest rates are one method it uses to guide the economy through rocky or smooth seas.

So, in order to encourage expenditure by making borrowing, including in money advance apps, less expensive when economic growth is poor, the Fed may cut interest rates. On the other hand, as the economy begins to expand, the Fed may raise interest rates in an effort to curb spending and prevent inflation.

When Do Interest Rates Fluctuate?

Your bank may alter the interest rate it pays on savings accounts at any moment because of the nature of variable rates. Some banks may provide promotional packages with fantastic interest rates that are only available while supplies last as incentives to attract new clients. When setting interest rates, banks often follow the Federal Reserve's example. The Federal Reserve modifies rates for a variety of economic factors, such as the COVID-19 pandemic in March 2020, which led them to lower interest rates to 0%. However, as you are well aware, this number has now steadied and even risen.

What Kinds of Savings Accounts Are There?

Checking, savings, and even investment accounts are just a few of the many kinds of bank accounts. There are two main sorts of accounts to search for when it comes to low-risk savings:

- Traditional savings accounts. These accounts are normally available at conventional brick-and-mortar banking institutions. If you already have a connection with the bank, traditional savings accounts are practical, but you'll get relatively little return on your money. These accounts now provide a meager 0.19% national average interest rate.

- High-yield savings accounts. These accounts are more often available at online banks or branches of bigger banking companies that exclusively operate online, although they provide substantially higher interest rates. Even with today's greatest rates, high-yield accounts still provide more than ten times the average return on a regular savings account.

How to Get Ready for Higher Savings Interest Rates

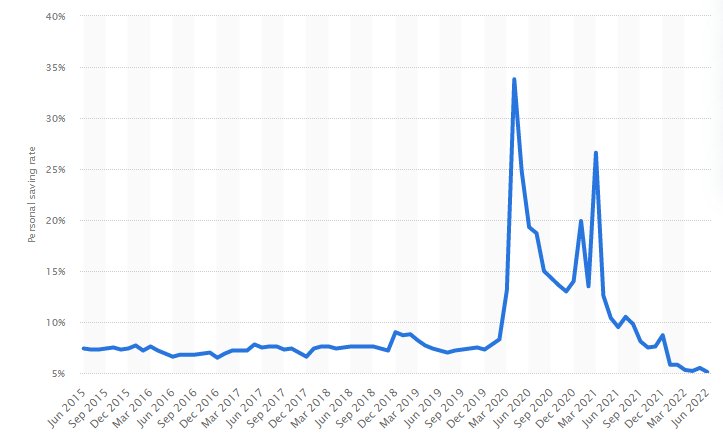

The personal saving rate in the US fell from 10.5 percent in July 2021 to 5.1 percent in June 2022. The personal saving rate is determined by dividing personal savings by available personal income.

This figure fell due to the weakening of the COVID-19 pandemic and rising inflation and higher prices. People are afraid and difficult to save money. However, you need to have a financial cushion, and here are some ways to be prepared for an interest rate hike.

Recognize Your Options

Different kinds of savings accounts exist. Although limited or no brick-and-mortar outlets are a frequent trade-off, high-yield savings accounts often provide higher interest rates than conventional savings accounts.

If you open a money market account or purchase a certificate of deposit, you could also find favorable rates. However, this may not be a suitable choice if you need regular access to your money.

Series I Bonds

Due to their capacity to match those rising expenses, Series I bonds have grown in popularity when inflation has reached record highs.

The current interest rate on Series I bonds is 9.62%, which experts agree is difficult to match elsewhere. If you make a purchase in the month of November, you will get 9.62% for the first six months and then an interest rate of possibly over 6% for the second six months.

However, Series I bonds also have disadvantages. The first year is the only time the funds may be withdrawn, and if you take them out before five years, you will forfeit three months' interest.

I bonds are undoubtedly something to think about in certain situations, but they shouldn't be used as a replacement for an emergency fund that is sufficiently stocked.

Prepare For Your Financial Demands

Even though online-only banks sometimes provide competitive interest rates, depositing and withdrawing funds may be challenging. The increased rate may not be worthwhile if you often make deposits or withdrawals of cash.

If switching is still advantageous, you'll need a strategy. One option is to put cash into a different checking or savings account with a bank that offers in-person services and then transfer the funds to the higher-interest savings account.

You might transfer funds back to the account that offers in-person services for withdrawals. You could also use an ATM. If you do, be sure you won't be assessed fees by your bank or the ATM; these costs might cancel out months' worth of interest in a single transaction.

If Possible, Pay Off Debts

Additionally, higher interest rates imply more costly loan and credit card payments. Before interest rates rise higher, savers with cash on hand should give paying off high-interest debt first priority.

If you have credit card debt that has to be paid off, switching to an interest-free plan is worthwhile. If you develop a plan and set up a direct debit to pay more than the minimum payback amount each month, you have plenty of time to pay off the debt.

Conclusion

Investing your money in a savings account eliminates all of your potential risks while yet allowing you to receive interest on your money. To help you build your savings, certain high-yield accounts provide interest rates that are much higher than the US average. Finding the ideal savings account for your financial objectives is doable since savers have a wide range of alternatives at their disposal.